Income Tax Overhaul: Major Tax Rule Changes Impacting Individuals

The taxation landscape in India is undergoing a monumental shift. In recent financial budgets, the Government of India has systematically introduced a slew of major reforms in the direct tax structure, fundamentally altering how individuals calculate, plan, and pay their income taxes. With the New Tax Regime firmly established as the default option, these rule changes are designed to simplify the overall tax system, maximize the disposable or take-home income for the middle class, and restructure the taxation of capital assets to create a unified, transparent framework.Navigating these changes is critical for every earning individual—whether you are a salaried professional, a retiree relying on pensions, a real estate owner, or an active investor in the stock market. From the expansion of income tax slabs and the enhancement of standard deductions to the complete overhaul of capital gains tax rates and the removal of indexation benefits on property, the financial rules of the game have been rewritten. Understanding these updates is no longer just about compliance; it is about strategically optimizing your personal finances, adapting to new investment realities, and accelerating your wealth-creation journey for the years to come.

Major Changes at a Glance

A. Revamped Tax Slabs and Allowances

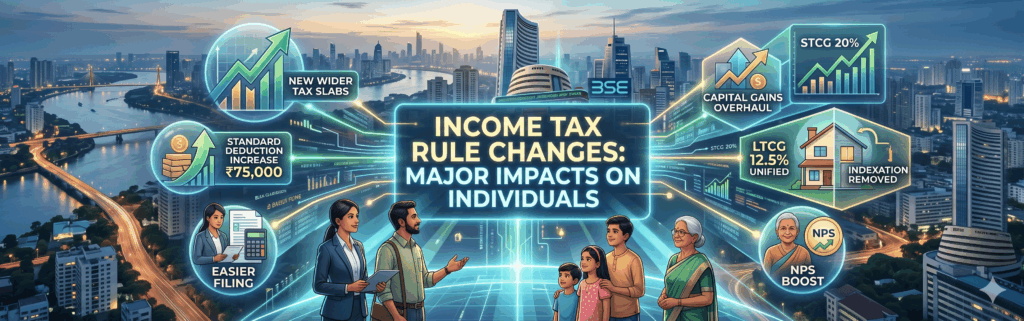

- ✓Widened Tax Brackets: The income slabs under the new tax regime have been expanded to provide greater relief. The 5% tax rate now applies to income between ₹3 lakh and ₹7 lakh, while the 10% rate covers ₹7 lakh to ₹10 lakh.

- ✓Enhanced Standard Deduction: A massive relief for the salaried class and pensioners—the standard deduction under the new regime has been increased by 50%, jumping from ₹50,000 to ₹75,000.

- ✓Family Pension Boost: For individuals relying on a family pension, the deduction limit has been increased from ₹15,000 to ₹25,000, ensuring more money remains in the hands of dependents.

- ✓Higher NPS Contributions: To encourage retirement savings, the deduction allowed for employer contributions to the National Pension System (NPS) has been increased from 10% to 14% of the employee’s basic salary under the new tax regime.

- ✓Default Status: The new, simplified tax regime is now the default. Taxpayers wishing to claim old exemptions (like 80C, HRA, or LTA) must consciously opt out.

B. Paradigm Shift in Capital Gains Taxation

- Increased STCG on Equities: The Short-Term Capital Gains (STCG) tax on specified financial assets (like listed equity shares and equity mutual funds) has been hiked from 15% to 20%, aiming to discourage short-term market speculation.

- Unified LTCG Rate: The Long-Term Capital Gains (LTCG) tax rate has been rationalized to a flat 12.5% for all financial and non-financial assets. This replaces the previous fragmented system where equities were taxed at 10% and real estate at 20%.

- Higher Exemption Limit: To protect small retail investors, the annual tax-free exemption limit on Long-Term Capital Gains has been increased from ₹1 lakh to ₹1.25 lakh.

- Removal of Indexation: The traditional indexation benefit (which allowed property sellers to adjust the purchase price for historical inflation) has been abolished for real estate and unlisted assets. Property sales will now attract a flat 12.5% tax on the actual profit.

C. Impact on Deductions and Wealth Building

- Diminishing Role of Section 80C: As the new tax regime becomes vastly more lucrative due to expanded slabs and standard deductions, traditional tax-saving instruments like ELSS, PPF, and Life Insurance premiums are losing their mandatory appeal for tax-saving purposes.

- Focus on Pure Investment Returns: Without the crutch of tax rebates, taxpayers are now encouraged to evaluate financial products strictly on their fundamental merits, risk profiles, liquidity, and inflation-beating returns.

- Streamlined Holding Periods: The holding period required for an asset to qualify as "long-term" has been simplified into two main categories: 12 months for listed securities and 24 months for all other assets (including real estate and gold).

Deep Dive: How the Revised Tax Slabs Work

To truly appreciate the benefit of the updated tax structures, one must look at the underlying math. Under the revised new tax regime, the basic exemption limit remains ₹3 lakh. However, the widening of subsequent brackets provides cascading monetary relief across almost all income levels. Here is how the progressive brackets operate: Income up to ₹3,00,000 attracts zero tax. Income from ₹3,00,001 to ₹7,00,000 is taxed at a minimal 5%. The ₹7,00,001 to ₹10,00,000 bracket is taxed at 10%, while income from ₹10,00,001 to ₹12,00,000 is taxed at 15%. The subsequent slab of ₹12,00,001 to ₹15,00,000 falls under the 20% bracket, and any income exceeding ₹15,00,000 continues to attract the highest marginal rate of 30%.Furthermore, the rebate under Section 87A ensures that individuals with a taxable income of up to ₹7 lakh effectively pay zero income tax. When you factor in the enhanced standard deduction of ₹75,000, a salaried individual earning up to ₹7.75 lakh in a financial year will have absolutely no income tax liability under the new regime. For middle and high-income earners, the widened slabs mean that a larger portion of their income is taxed at lower brackets, resulting in direct tax savings of up to ₹17,500 annually compared to the previous iteration of the new regime.

Decoding the Capital Gains Overhaul

The changes to capital gains taxation represent one of the most fundamental shifts in the Indian tax code in recent decades. The government's philosophy here is twofold: simplify the tax brackets across different asset classes to prevent arbitration, and deter excessive short-term speculative trading in the stock market. By increasing the Short-Term Capital Gains (STCG) tax on equity from 15% to 20%, day traders, swing traders, and short-term mutual fund investors face a notably higher tax burden. This policy actively nudges the retail population toward patient, long-term investing.On the long-term front, unifying the tax rate at 12.5% for both financial assets (like stocks and mutual funds) and non-financial assets (like real estate and physical gold) brings a much-needed parity to the system. Previously, calculating real estate capital gains was a complex affair involving the Cost Inflation Index (CII) to adjust the purchase price. By eliminating indexation, the calculation is radically simplified: you simply subtract the original purchase price from the sale price and apply a 12.5% tax to the profit.

What Taxpayers Should Do?

- Compare the Regimes Annually: Do not blindly default to the new tax regime. If you have significant ongoing deductions like a large home loan interest payout, high HRA, and full 80C utilization, use an income tax calculator to mathematically compare your liability under both regimes before filing.

- Claim the Higher Standard Deduction: Ensure your employer has updated their payroll processing systems to factor in the ₹75,000 standard deduction so that your monthly TDS is reduced accordingly.

- Re-evaluate Real Estate Strategies: If you are planning to sell a property, consult a chartered accountant or tax advisor to calculate the exact impact of the removal of indexation on your specific transaction to avoid surprise tax liabilities.

- Optimize NPS Contributions: Take full advantage of the increased 14% employer contribution limit to the National Pension System to securely build a robust retirement corpus while legally minimizing your taxable income.

- Rethink Equity Holding Periods: With STCG raised to 20%, reconsider your trading frequency. Holding fundamentally strong stocks and mutual funds for over 12 months is now significantly more tax-efficient.

Big Picture

The latest income tax reforms reflect a decisive push towards a simpler, compliance-friendly, and exemption-free tax ecosystem. By sweetening the new tax regime with wider brackets and higher standard deductions, the government is successfully weaning taxpayers off complex, paperwork-heavy deductions that often caused litigation and assessment delays. Concurrently, the rationalization of capital gains tax brings structural parity across diverse asset classes, encouraging long-term wealth creation while actively curbing short-term market speculation. Although the transition—especially the sudden removal of property indexation—may pose localized challenges for long-time real estate investors, the overarching outcome is a more transparent, robust, and equitable tax environment. For the average citizen, this translates into higher monthly disposable income, less administrative hassle during tax season, and a clearer runway for independent, goal-based financial planning.✓ Takeaway: For individuals, this is the crucial moment to reassess financial portfolios, pivot away from investments driven solely by tax-saving motives, and embrace the simpler tax slabs. For investors and property owners, adjusting your asset holding periods and fully understanding the new 12.5% unified long-term capital gains tax rate will be the key to maximizing your post-tax returns.

Latest Blog