Income Tax Forms Reorganized Under New Act: What You Need to Know

For years, taxpayers and financial professionals have grappled with the complexity of choosing the right Income Tax Return (ITR) form. From ITR-1 for simple salaried income to ITR-3 and ITR-4 for complex business and professional earnings, the numerical soup of forms often led to filing errors, defective returns, and unnecessary anxiety. Recognizing this friction, the Income Tax Department, under the latest provisions of the revised Direct Tax Act, has completely reorganized and streamlined the ITR forms.This overhaul is not just a cosmetic name change; it is a fundamental shift towards a technology-driven, user-centric filing experience. By consolidating the legacy forms into a smart, dynamic system, the tax department aims to drastically reduce the compliance burden, minimize errors, and make the annual tax filing process as intuitive as answering a simple questionnaire. Whether you are a salaried employee, a freelancer, a small business owner, or an active stock market trader, understanding this new form architecture is essential for a smooth, hassle-free tax season.

Major Changes at a Glance

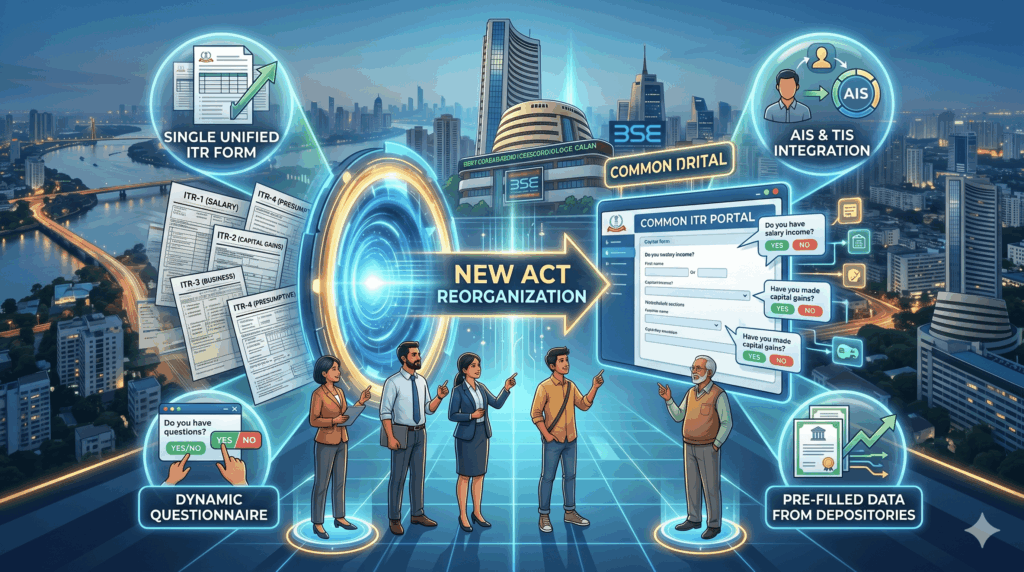

A. The Shift to a Dynamic "Common ITR"

- ✓Consolidation of Old Forms: The traditional standalone forms (ITR-1, ITR-2, ITR-3, ITR-4, ITR-5, and ITR-6) have been heavily consolidated. Instead of choosing a specific form based on your income type, most taxpayers will now use a unified "Common ITR."

- ✓Smart Questionnaire Mechanism: The new filing portal asks a series of simple 'Yes/No' questions (e.g., "Do you own a business?", "Did you sell any mutual funds this year?"). Based on your answers, the form dynamically generates only the schedules and sections relevant to you.

- ✓Reduced Clutter: By hiding irrelevant schedules (like foreign asset disclosures for a local salaried worker), the visual clutter is significantly reduced, saving time and preventing confusion.

- ✓ITR-7 Remains Separate: For charitable trusts, political parties, and other specialized institutions, the traditional ITR-7 form continues to exist separately from the Common ITR structure.

B. Enhanced Pre-filling and Data Integration

- Seamless AIS Integration: The Annual Information Statement (AIS) and Taxpayer Information Summary (TIS) are now deeply integrated into the new forms. Data regarding salary, interest, dividends, and high-value transactions are automatically populated.

- Broker & Exchange Sync: For investors, capital gains data from major stockbrokers and depositories will be directly imported into the respective schedules, eliminating the need for manual, row-by-row data entry of trades.

- Auto-Reconciliation: The new system actively cross-checks the declared income against the data available with the IT department, instantly flagging discrepancies before final submission to prevent future notices.

C. Impact on Different Taxpayers

- Salaried Individuals: The process becomes virtually one-click for those with only salary and bank interest, as the dynamic logic will bypass all complex business and capital gains schedules.

- Freelancers & Gig Workers: The transition is highly beneficial. Professionals no longer need to navigate the intimidating full-scale business ITR-3; the dynamic form will simply open the specific presumptive taxation (Section 44ADA) schedules for them.

- Crypto & Virtual Asset Investors: A dedicated, simplified schedule for Virtual Digital Assets (VDAs) has been integrated, making it easier to declare crypto profits and pay the flat 30% tax without disrupting other income declarations.

Decoding the "Schedule-Based" Architecture

The underlying philosophy of the new reorganized forms is a shift from a "Form-based" approach to a "Schedule-based" approach. In the past, if a salaried person accidentally made one small freelance invoice, they had to abandon the simple ITR-1 and fill out the massive ITR-3 or ITR-4, exposing themselves to dozens of irrelevant pages.Under the new architecture, the base of the tax return remains identical for everyone: a core module capturing basic demographic details, total income summary, and final tax computation. Attached to this core are various "Schedules" (e.g., Schedule Salary, Schedule House Property, Schedule Capital Gains, Schedule Business/Profession). You only interact with the schedules triggered by your specific income profile. This modular design not only accelerates the filing process but also drastically reduces the server load on the e-filing portal, ensuring a smoother experience even during the peak deadline rush.

What Taxpayers Should Do?

- Review Your AIS Early: Because the new forms rely heavily on pre-filled data, it is absolutely critical to download and verify your Annual Information Statement (AIS) by May or June. If there are errors in the department's data, you must raise a correction request before filing.

- Answer the Questionnaire Carefully: Do not rush through the initial 'Yes/No' prompts. Answering incorrectly might hide a schedule you need (leading to under-reporting) or open schedules you don't (causing confusion).

- Link All Bank Accounts: Ensure all your active bank accounts are linked and validated on the e-filing portal to ensure seamless processing of potential refunds through the unified form.

- Consult Your CA for Complex Transitions: If you have brought forward losses from previous years under old forms (like ITR-2 or ITR-3), consult a tax professional to ensure those losses are correctly mapped to the new Common ITR schedules.

Big Picture

The reorganization of income tax forms under the new Act is a landmark step towards global best practices in tax administration. By adopting a dynamic, unified form structure, the government is actively removing the intimidation factor associated with tax filing. This reform pairs perfectly with the simplified New Tax Regime slabs, collectively driving a dual agenda: ease of doing business and ease of living. While the initial transition might require taxpayers to familiarize themselves with the new interface, the long-term result will be a faster, cleaner, and highly transparent tax compliance ecosystem that benefits both the citizen and the state.✓ Takeaway: Embrace the change. The era of choosing between ITR-1, 2, 3, or 4 is ending. Taxpayers should focus on maintaining clean financial records, verifying their pre-filled AIS data early, and utilizing the smart new Common ITR to file returns accurately and stress-free.

Latest Blog